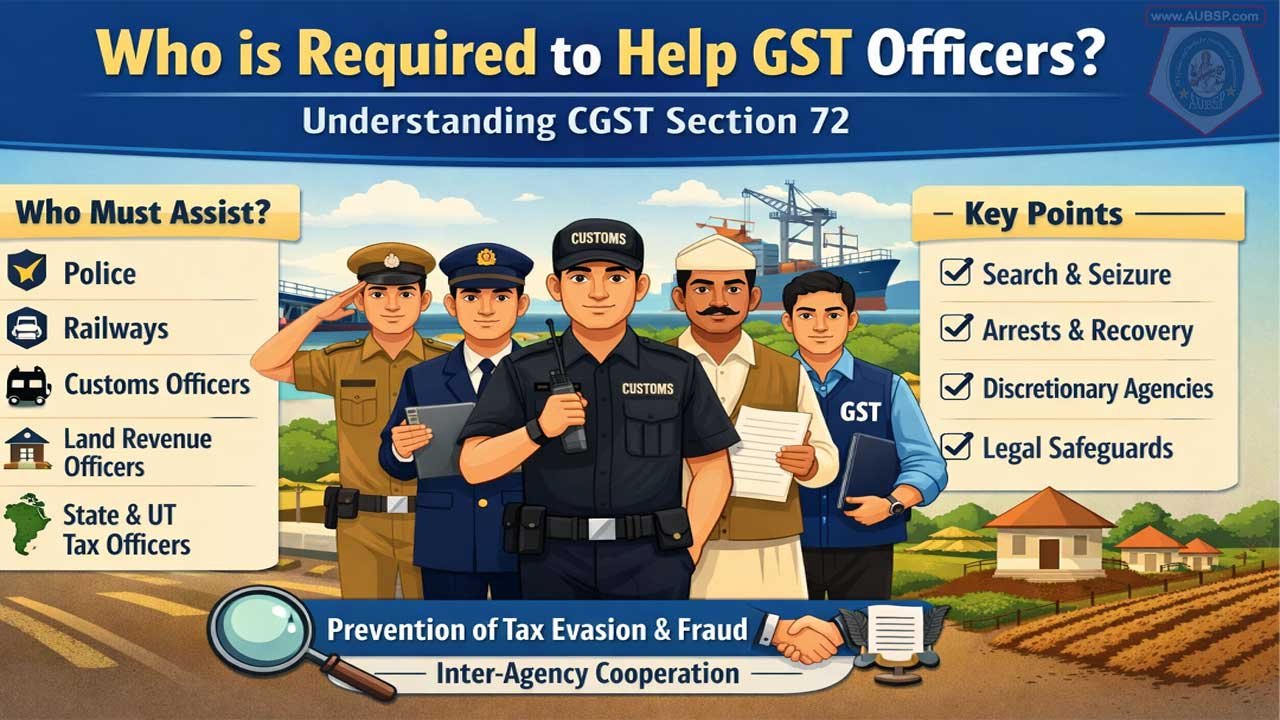

Section 72 of the CGST Act, 2017 ensures that GST officers receive mandatory help from other government departments like Police, Railways, Customs, and Land Revenue for effective tax enforcement.

It creates a legal duty for these officers to assist in search, seizure, arrest, recovery, and verification activities. The law also allows the government to notify other agencies when needed. This cooperation helps prevent tax evasion, fake firms, and fraud. However, these powers must follow legal safeguards like written authorization and “reason to believe.”

Courts ensure that officers do not misuse their authority and that genuine taxpayers are protected. Overall, Section 72 strengthens GST enforcement through coordinated government action while maintaining legal checks and balance.

| Aspect | Information |

|---|---|

| Section | Section 72, CGST Act, 2017 |

| Title | Officers to Assist Proper Officers |

| Purpose | Ensures inter-departmental cooperation for GST enforcement |

| Mandatory Assistance (72(1)) | Police, Railways, Customs, Land Revenue, State & UT Tax Officers |

| Nature of Duty | Statutory and compulsory (“shall” indicates mandatory) |

| Discretionary Power (72(2)) | Govt. may notify other officers/agencies to assist |

| Used During | Search, seizure, arrest, inspection, recovery proceedings |

| Legal Safeguard | Requires “reason to believe” and written authorization |

| Penalty for Obstruction | Penalty under Section 122; IPC Sections 186 & 187 may apply |

| Objective | Strengthen enforcement through coordinated government action |

The Statutory Mandate of Inter-Agency Cooperation: An Exhaustive Analysis of CGST Section 72

The implementation of the Central Goods and Services Tax (CGST) Act, 2017, marked a watershed moment in the Indian fiscal landscape, consolidating a fragmented indirect tax structure into a unified, destination-based consumption levy. This transition necessitated not only a robust internal administrative framework but also a legislative mechanism to ensure that tax authorities could leverage the resources and specialized capabilities of other government departments.

Section 72 of the CGST Act, titled “Officers to assist proper officers,” serves as the critical legal bridge facilitating this inter-departmental synergy. By mandating cooperation from agencies such as the Police, Railways, Customs, and Land Revenue departments, the Act ensures that the enforcement of tax laws is a coordinated effort of the entire state apparatus, rather than the isolated burden of a single ministry.

Legislative Context and the Genesis of Section 72

The CGST Act was enacted on 12th April 2017 to make provisions for the levy and collection of tax on intra-State supply of goods or services. From its inception, the legislation recognized that the “proper officers”—those authorized by the Commissioner to perform specific functions—would frequently operate in environments where their specific training in tax law might not suffice to manage physical, logistical, or security challenges. Section 72 was specifically designed to address these gaps, ensuring that the implementation of the Act remains effective even in the face of active resistance, cross-border complexities, or rural logistical hurdles.

The enforcement date for Section 72 was 1st July 2017, coinciding with the broader launch of the GST regime. Its inclusion in Chapter XIV, alongside provisions for inspection, search, seizure, and arrest (Sections 67 to 71), highlights its primary function as an enforcement-support tool. The legislative structure suggests that while tax officers are the lead investigators, the agencies listed in Section 72 provide the necessary infrastructure and authority to execute these investigations safely and comprehensively.

Structural Analysis of Section 72

Section 72 is characterized by a two-pronged approach to administrative assistance, distinguishing between mandatory statutory obligations and discretionary executive empowerments.

Mandatory Statutory Duty under Subsection 1

Subsection (1) creates an immediate and permanent legal obligation for specific classes of officers to assist proper officers. The use of the word “shall” indicates that this is not an optional or discretionary request but a statutory command. The categories of officers listed under this subsection represent the primary touchpoints of physical and economic movement in India:

- Officers of Police: Essential for maintaining order during search operations and executing arrests.

- Officers of Railways: Critical for monitoring the movement of goods and intercepting non-compliant shipments.

- Officers of Customs: Vital for ensuring the integrity of the import-export chain and preventing circular trading.

- Officers engaged in the collection of land revenue: This includes village officers, whose local knowledge is indispensable for identifying “ghost” business premises in remote areas.

- Officers of State Tax and Union Territory Tax: This ensures a seamless flow of assistance across the federal structure, preventing jurisdictional silos from impeding investigations.

Discretionary Empowerment under Subsection 2

Subsection (2) provides the Central Government with the flexibility to expand the pool of available assistance through notifications. Under this provision, the Government may empower any other class of officers to assist proper officers when “called upon to do so by the Commissioner”.

This allow the integration of specialized agencies—such as the Serious Fraud Investigation Office (SFIO), the Central Bureau of Investigation (CBI), or digital platform administrators—into the GST enforcement framework as specific needs arise.

| Statutory Provision | Target Officers | Nature of Obligation | Trigger Mechanism |

|---|---|---|---|

| Section 72(1) | Police, Railways, Customs, Land Revenue, State/UT Tax Officers | Mandatory and Permanent | Direct statutory command |

| Section 72(2) | Any other notified class (e.g., SFIO, specialized agencies) | Contingent and Specific | Notification followed by Commissioner’s call |

Functional Integration: How Assistance is Rendered

The assistance provided under Section 72 is not a vague concept of cooperation but translates into specific, high-impact actions during the various stages of tax enforcement.

Assistance in Inspection, Search, and Seizure (Section 67)

The most prominent use of Section 72 assistance occurs during search and seizure operations conducted under Section 67. When a Joint Commissioner has “reasons to believe” that a taxpayer has suppressed information or evaded tax, they authorize a search via FORM GST INS-01. In such scenarios, the practical role of assisting officers is multi-faceted:

- Maintaining Public Order: Police officers cordon off premises and manage any physical resistance or crowd gathering that might obstruct the proper officer.

- Executing Forced Entry: Section 67(4) empowers officers to “break open” doors or almirahs where access is denied. Police assistance is often required to exercise this power safely and legally.

- Witness Identification: Search proceedings must be witnessed by at least two independent inhabitants of the locality. Local village officers or police often facilitate the identification and presence of these witnesses to ensure the search’s legal validity.

- Inventory Management: Assisting officers help in the physical handling and securing of seized goods, documents, and electronic devices, ensuring that the chain of custody remains intact.

Role of Railway Officers in Logistics Monitoring

Railway officers provide a specialized form of assistance related to the movement of goods in transit. Under Section 68, the Government may require the person in charge of a conveyance carrying goods to carry specific documents, such as an e-way bill or tax invoice.

Railway officers assist proper officers by:

- Physical Weighment: Assisting in the 100% weighment of container rakes when there is suspicion of undeclared payload or misclassification of goods.

- Documentation Verification: Checking railway receipts (RR) against GST declarations to detect discrepancies in consignor or consignee information.

- Site Inspections: Monitoring work-in-progress and the movement of raw materials along railway tracks, which is often crucial for verifying large-scale construction or infrastructure projects.

Grassroots Intelligence and Land Revenue Recovery

The inclusion of land revenue and village officers in Section 72(1) is a strategic acknowledgment of the importance of “feet on the street”. These officers serve as the ultimate link in the enforcement chain, especially in rural or semi-urban areas.

- Physical Verification of Business: When the GST department suspects a “ghost firm” is operating only on paper, village officers provide the physical confirmation of whether the registered person actually occupies the declared premises.

- Recovery of Dues: Under Section 79, one of the methods for recovering tax dues is by “attachment and sale of immovable property.” Land revenue officers are the primary authority for maintaining land records and executing such attachments, ensuring that the government’s claim is properly recorded in the revenue books.

- Intelligence Gathering: These officers often have insights into local market dynamics and suspicious movements of goods that might not be captured by electronic data analysis alone.

The Legal Threshold: “Reason to Believe” and Procedural Safeguards

The exercise of enforcement powers, and by extension the call for assistance under Section 72, is governed by strict legal thresholds to protect the rights of genuine taxpayers. The core requirement is the existence of a “reason to believe”.

Defining “Reason to Believe”

Judicial interpretation has clarified that “reason to believe” is not a subjective opinion but a determination based on an intelligent examination of facts. It must be based on relevant material and circumstances that would cause an honest and reasonable person to conclude that there is a contravention of the law. Proper officers cannot call for police assistance or conduct searches based on mere suspicion or whims.

Procedural Formalities and Documentation

To ensure accountability, several procedural safeguards are embedded in the GST Rules and instructions:

- Authorization in Writing: Any officer conducting a search or seizure must have a written authorization (INS-01) from an officer not below the rank of Joint Commissioner.

- Document Identification Number (DIN): In accordance with CBIC instructions, all formal communications, including search authorizations, must bear a system-generated DIN to prevent unauthorized or back-dated actions.

- The Panchnama: Every search operation must culminate in a Panchnama—a detailed record of the proceedings, signed by the witnesses and the person in charge of the premises. Assisting officers from the police or other departments often sign as part of the team to validate the transparency of the process.

Challenges in Inter-Departmental Cooperation: The “Proper Officer” Discordance

A significant area of contemporary legal dispute involves the determination of who constitutes a “proper officer” for the purpose of initiating investigations and, consequently, calling for assistance under Section 72.

The Role of DGGI and Jurisdictional Issues

The Directorate General of GST Intelligence (DGGI) frequently conducts intelligence-based enforcement actions against taxpayers who are administratively assigned to State tax authorities. While the Board has clarified that officers of both Central and State tax are authorized to take such actions irrespective of administrative assignment, taxpayers have frequently challenged the jurisdiction of Central officers to initiate proceedings on matters assigned to the State.

The case of DGGI Meerut Zonal Unit highlighted the complexities of this cross-empowerment. The court observed that while intelligence-based actions are permissible across the value chain, the authority that initiates the action is empowered to complete the entire process—including investigation, issuance of a show-cause notice (SCN), and recovery. This implies that if a Central officer initiates a search with police assistance under Section 72, they remain the jurisdictional authority for that specific case.

Avoiding Parallel Proceedings

A key protection for taxpayers is the bar on parallel proceedings. Section 6(2)(b) of the CGST Act stipulates that once a proper officer of the State tax has initiated proceedings on a subject matter, no proper officer of the Central tax shall initiate proceedings on the same subject matter. Courts have held that “proceedings” in this context refers to formal actions like adjudication or assessment, but investigations and summonses are precursors and do not necessarily trigger this bar unless the specific tax liability and facts are identical.

Penalties and the Deterrent Effect of Section 72

The effectiveness of Section 72 as a support mechanism is reinforced by a rigorous penalty framework for those who obstruct or fail to cooperate with GST officers.

Penalty for Obstruction

Under Section 122(1)(xiii), any person who “obstructs or prevents any officer in discharge of his duties under this Act” is liable to a penalty. This applies not only to the taxpayer but also to third parties who might interfere with a search operation or refuse to comply with a lawful order from an assisting police officer.

| Nature of Default | Relevant Section | Penalty Amount |

|---|---|---|

| Obstruction of Officer | 122(1)(xiii) | Higher of $₹10,000$ or tax evaded |

| Failure to attend summons | 122(3)(d) | Up to $₹25,000$ |

| Falsifying records to evade tax | 122(1)(x) | Higher of $₹10,000$ or tax evaded |

| Failure to furnish information return | 123 | $₹100$ per day (Max $₹5,000$) |

| General Penalty (No specific penalty) | 125 | Up to $₹25,000$ |

Integration with Criminal Law (IPC and BNS)

The mandate of Section 72 is further supported by the Indian Penal Code (IPC). Since Section 72 creates a legal obligation for officers to assist, a failure to do so could be considered a criminal omission.

- Section 186 of the IPC: Specifically punishes the voluntary obstruction of a public servant in the discharge of their public functions.

- Section 187 of the IPC: Punishes the omission to assist a public servant when bound by law to do so. This is directly applicable to the officers listed in Section 72 who might neglect their duty to support GST proper officers.

Furthermore, the Act provides for prosecution and arrest in severe cases of fraud or high-value tax evasion. If a person collects tax but fails to pay it to the government for more than three months, or if they fraudulently avail ITC using fake invoices, the Commissioner can authorize their arrest. Police assistance under Section 72 is fundamental in executing these arrests and producing the accused before a Magistrate within 24 hours.

Judicial Precedents: Shaping the Scope of Inter-Agency Support

The judiciary has played a crucial role in ensuring that the powers granted under Section 72 and the related enforcement sections are exercised within the bounds of constitutional and administrative law.

The Sudhakar Traders Decision: Inherent Rights vs. Mandated Requisition

In M/S. Sudhakar Traders versus The State of Andhra Pradesh, the Andhra Pradesh High Court addressed the relationship between independent investigative departments and the GST authorities. The court held that the Vigilance and Enforcement (V&E) Department has a statutory right to conduct inspections and share information with the Commercial Tax Department even without a specific requisition under Section 72(2). This ruling clarifies that Section 72 is a tool for cooperation, not a restrictive boundary that prevents other agencies from performing their legitimate duties in the interest of revenue protection.

The Armour Security Test: Defining “Same Subject Matter”

In M/S Armour Security India Pvt Ltd v. Commissioner CGST, the Supreme Court established a two-fold test to determine if a subsequent inquiry is barred by an existing one:

- Whether the authority has already acted on an identical tax liability on similar facts.

- Whether the relief sought is identical.

This case confirmed that overlapping aspects of inquiries do not make the “subject matter” identical unless a formal show-cause notice has specified the liability. This gives investigating authorities, and the assisting agencies under Section 72, the necessary latitude to conduct comprehensive searches and gather intelligence without fear of being immediately blocked by a prior minor inquiry.

Protecting the Bona Fide Purchaser

The courts have also intervened to balance the department’s enforcement powers with the rights of innocent businesses. In cases where Input Tax Credit (ITC) is denied because a supplier is found to be non-existent, judicial pronouncements have emphasized that bona fide purchasers who have exercised due diligence should not be penalized for the supplier’s default. This indicates that while Section 72 allows for powerful enforcement actions (like searching a purchaser’s premises), the results of those actions must be applied fairly, respecting the principles of justice inherent in GST law.

Digital Transformation and the Future of Section 72

The “officers” mentioned in Section 72 are no longer limited to physical personnel. The concept of “assistance” is rapidly evolving into a framework of digital data exchange and automated risk management.

The Role of Technology Platforms

Subsection (2) of Section 72 has been used to notify digital systems as entities that must assist the tax administration. A notable example is the notification of the “Public Tech Platform for Frictionless Credit” as a system with which the GST common portal may share information. This allows for a two-way flow of data, where the platform assists the GST department in verifying the creditworthiness and compliance of taxpayers, while the department assists the platform by providing validated tax data.

Intelligence-Led Enforcement (DGARM and BI Tools)

Modern enforcement is driven by sophisticated data analytics. The Directorate General of Analytics and Risk Management (DGARM) and Business Intelligence (BI) tools developed by GSTN allow proper officers to identify high-risk taxpayers with surgical precision.

- Red Flag Generation: These tools identify mismatches between GSTR-1, 3B, and E-way bill data.

- Targeted Intervention: Once a high-risk case is identified, the proper officer can call for specific assistance under Section 72—such as a railway weighment check or a physical verification by a village officer—to confirm the digital suspicion.

This shift from “general surveillance” to “targeted intelligence” makes the assistance mandated by Section 72 more efficient, reducing the burden on assisting departments and minimizing the disruption for compliant businesses.

Standard Operating Procedures for Inter-Departmental Synergy

To ensure uniformity and prevent the misuse of power, the CBIC and the GST Council have issued comprehensive manuals and instructions, such as the Model All India GST Audit Manual.

Guidelines for Audit and Scrutiny

The manual emphasizes that unless the processes of selection and investigation are grounded in neutrality and transparency, the purpose of the law is not served. Audit officers are encouraged to use the “BI Tools” and “Registered Person Master File” (RPMF) to prepare their cases before ever stepping into a taxpayer’s premises. When an audit reveals discrepancies that suggest tax evasion, the transition to a search operation (under Section 67) involves a formal hand-off to the enforcement wing, which then invokes Section 72 for police or logistical support.

Scrutiny Parameters and Reconciliation

Officers are provided with an indicative list of parameters for scrutiny, including:

- GSTR-1 vs 3B reconciliation.

- ITC from ISD (Input Service Distributor) vs 2A/2B.

- Outward supplies vs E-way bill data.

If these reconciliations show significant gaps, the department can utilize Section 72 to verify the physical reality behind the numbers—for example, asking land revenue officers to check the stock of goods in hand at a specific warehouse.

Conclusion: Section 72 as a Pillar of Cooperative Federalism

The analysis of Section 72 of the CGST Act reveals it to be much more than a procedural requirement for inter-departmental cooperation. It is a fundamental pillar of the GST enforcement architecture, designed to ensure that the “one nation, one tax” vision is supported by a “whole-of-government” enforcement strategy.

The mandatory assistance from the Police, Railways, Customs, and Land Revenue departments provides the physical security, logistical oversight, and grassroots intelligence necessary to tackle sophisticated tax fraud. Meanwhile, the discretionary power under subsection (2) ensures that the law can adapt to the digital age, integrating technology platforms and specialized agencies into the tax administration’s toolkit.

However, the power granted under Section 72 is not absolute. It is tempered by judicial oversight, procedural formalities (like DIN and INS-01), and the strict “reason to believe” threshold. The ongoing disputes regarding “proper officers” and jurisdictional boundaries serve as healthy reminders of the need for continuous legal refinement and clear executive notifications.

In summary, Section 72 represents the practical realization of cooperative federalism in the fiscal sphere. It acknowledges that the protection of government revenue is a collective duty of all state functionaries. For the taxpayer, it signifies the comprehensive reach of the department’s investigative powers. For the state, it provides the structural integrity needed to maintain a fair, transparent, and compliant tax ecosystem in a complex and evolving economy.

Leave a Reply

You must be logged in to post a comment.