The Ministry of Corporate Affairs (MCA) has brought a welcome sigh of relief to corporate professionals and businesses. Through General Circular No. 02/2026, issued on June 19, 2026, the MCA has officially relaxed the requirement to pay additional fees for the delayed filing of Form DPT-3 for the financial year ending March 31, 2026.

Here is a breakdown of what this circular means, why the extension was granted, and what companies need to do next.

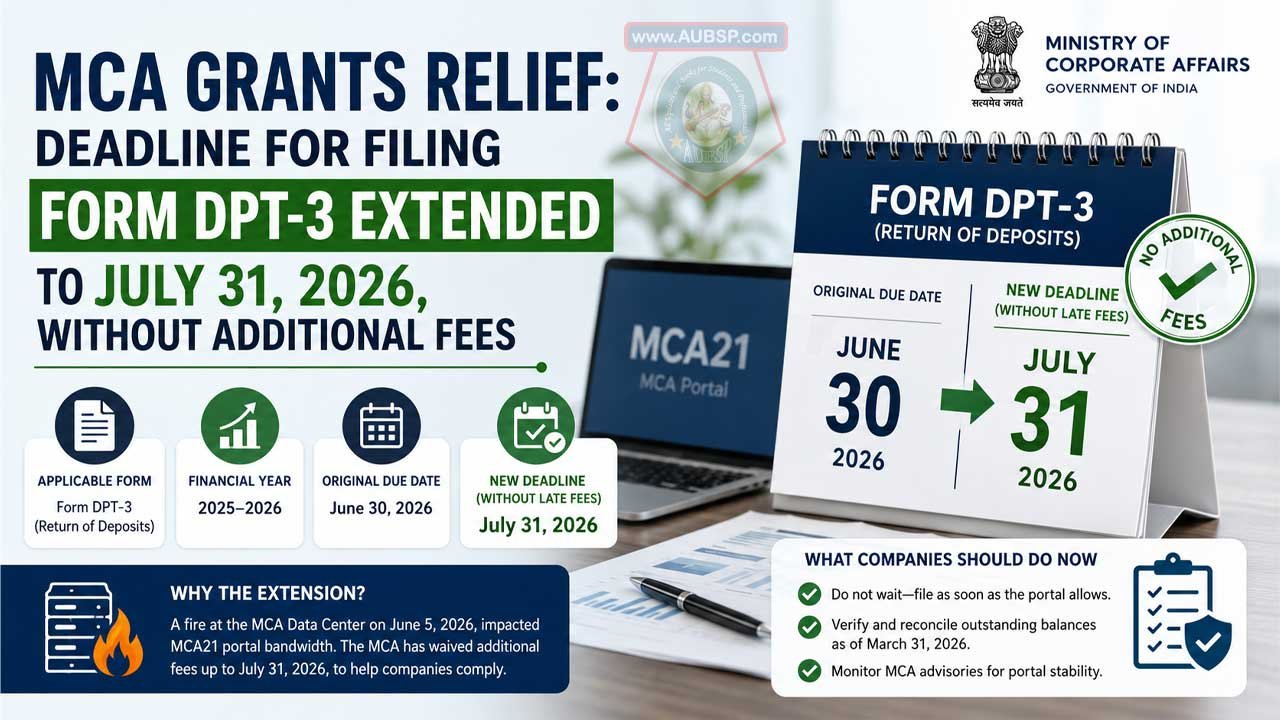

Key Highlights of the Circular

The MCA has provided a one-month grace period for compliance. During this window, companies can file their return of deposits without incurring the standard late penalties.

| Detail | Particulars |

|---|---|

| Applicable Form | Form DPT-3 (Return of Deposits) |

| Applicable Financial Year | 2025–2026 |

| Original Due Date | June 30, 2026 |

| New Deadline (Without Late Fees) | July 31, 2026 |

| Circular Reference | General Circular No. 02/2026 |

Why the Extension?

The original deadline for filing Form DPT-3 is always June 30th of the corresponding assessment year. However, the MCA acknowledged recent infrastructural hurdles affecting the MCA21 portal.

On June 5, 2026, a fire incident occurred at the MCA Data Center. While core data remains secure, the resulting capacity enhancement and ongoing system restoration activities have impacted the portal’s bandwidth. Anticipating that these technical disruptions would prevent companies from filing smoothly by the end of June, the MCA proactively waived the additional fees through July 31, 2026.

A Quick Refresher: What is Form DPT-3?

For those newer to corporate compliance, Form DPT-3 is a mandatory annual return filed by companies to report their deposit liabilities and any outstanding receipts that are not considered deposits.

- Who must file? All companies—including private limited, public limited, and one-person companies (OPCs)—must file this form if they have any outstanding loans, advances, or deposits as of March 31st.

- Who is exempt? Government companies, Non-Banking Financial Companies (NBFCs) registered with the RBI, and housing finance companies are generally exempt from this specific filing.

- Auditor’s Role: If the company is reporting actual deposits, an auditor’s certificate must be attached to the form.

What Should Companies Do Now?

While the waiver of additional fees up to July 31st is a helpful buffer, the underlying system restoration at the MCA Data Center means that the portal may still experience intermittent sluggishness.

- Do not wait for the new deadline: Use this extra time to gather your auditor certificates and reconcile your financial statements, but attempt to file as soon as the portal allows. Traffic will inevitably spike again in late July.

- Verify Outstanding Balances: Ensure that any loans from directors, inter-corporate deposits, or business advances are accurately classified and reconciled as of March 31, 2026.

- Monitor the Portal: Keep an eye on MCA advisories regarding portal stability to plan your actual submission time.

Leave a Reply

You must be logged in to post a comment.